Mortgages Surge During the Pandemic

We learn a lot about the mortgage market by understanding why it defied expectations during the pandemic.

Natalie Newton

Research Analyst

FEDERAL RESERVE BANK OF PHILADELPHIA

James Vickery

Senior Economic Advisor and Economist

FEDERAL RESERVE BANK OF PHILADELPHIA

The views expressed in this article are not necessarily those of the Federal Reserve.

The U.S. mortgage market experienced a surprising boom in 2020 and 2021, with new lending reaching an all-time high in excess of $4 trillion per year. The boom is particularly striking in light of the challenges the mortgage market faced as the COVID-19 pandemic took hold in the U.S. in March 2020. The emergence of the virus led to financial market disruptions and a short but deep recession, prompting concerns about a potential spike in mortgage defaults and foreclosures and the possible failure of mortgage lenders and servicers. Understanding the mortgage boom is important because mortgages are by far the largest component of household debt and because mortgage market conditions significantly affect the housing market, household spending, and financial stability.

In this article, we present facts about the pandemic mortgage boom and discuss the reasons why the mortgage market was able to prosper during a period of such economic uncertainty. We find that record-low interest rates, a relatively rapid economic recovery, and surging home prices all contributed in important ways to the lending boom. Underlying these outcomes, government policy actions, including expansionary monetary and fiscal policy and policies to stabilize mortgage intermediaries, played a significant role in supporting the mortgage and housing markets.

We also highlight some important limits of the boom. First, the mortgage industry faced significant capacity constraints as originators scrambled to expand lending in a challenging operating environment. As a result, only part of the decline in financial market yields was passed along to mortgage borrowers in the form of lower interest rates. (Yield in this context refers to the rate of return over the life of a fixed-income security such as a Treasury bond or mortgage-backed security.) In other words, although fixed mortgage rates fell to record lows below 3 percent in 2020 and 2021, rates could have been even lower if the credit supply

had been more elastic.

Second, the low-rate environment did not benefit all mortgage borrowers equally. Mortgage rates did not fall as much for certain types of loans, such as those for large “jumbo” mortgages not eligible for government-backed credit guarantees. Black, Latino,, and Asian borrowers were less likely to refinance and thereby benefit from lower mortgage rates. This inequality in refinancing opportunities highlights the potential benefits of alternative mortgage contracts designed to allow mortgage rates to decline automatically along with market rates, sparing the borrower from needing to refinance.

The Boom in Context

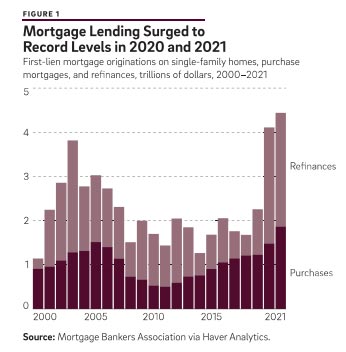

Lenders originated $4.1 trillion in new mortgage loans in 2020, a new record and much higher than nominal lending volume in any year since 2003 (Figure 1). The torrid pace of lending continues in 2021, with an even higher $4.4 trillion of originations.’

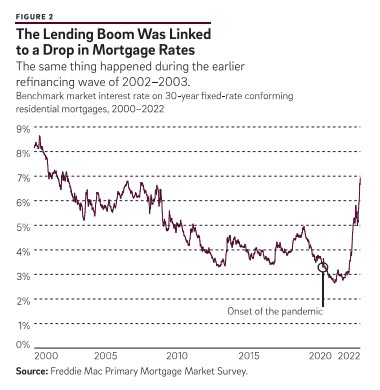

This surge in lending was closely connected to lower mortgage interest rates. The Freddie Mac benchmark 30-year fixed mortgage rate fell below 3 percent for the first time in July 2020 and remained at or close to its all-time low through the rest of 2020 and 2021 (Figure 2).?

A drop in mortgage rates boosts lending through two main channels. First, it incentivizes borrowers to refinance their existing mortgages at the new, lower market interest rates. Reflecting this incentive, refinancing more than doubled from 2019 to 2020,

from $1.0 trillion to $2.6 trillion, accounting for the majority of the total rise in mortgage lending.? Second, lower interest rates increase homebuyers’ purchasing power, likely providing a tailwind for the housing market, particularly as the economy started to show signs of recovery.‘ This was reflected in a smaller but still significant increase in the volume of “purchase mortgage” lending—that is, lending used to finance a home purchase.

Subsequently, the path of mortgage interest rates abruptly changed course in 2022—the benchmark 30-year fixed mortgage The interest rate rose from 3.1 percent at the end of 2021 to 6.9 percent in October 2022, a level of rates not seen since 2002. Recent data suggests this sharp rise in borrowing costs has significantly curtailed mortgage lending activity, particularly for refinancing. Mortgage Bankers Association data indicate that applications for mortgage refinances in September 2022 were 84 percent lower than in the same month of 2021, while purchase applications were 30 percent lower. Similarly, total mortgage lending in the second quarter of 2022 was down by 42 percent relative to the second quarter of 2021. In short, it seems clear that the mortgage boom of 2020–2021 has now come to an end.

Initial Fears About the Mortgage Market

With the benefit of hindsight, 2020–2021 was a banner period for the mortgage market, but at the onset of the CovID-19 pandemic in March 2020, the mortgage the outlook seemed highly uncertain, with the market apparently facing significant headwinds.

One concern was that the pandemic seemed to presage a challenging period for the housing market. Who would buy homes in such an uncertain environment? How would lenders conduct appraisals, inspections, and closings during a period of lockdowns and social distancing?

Financial markets were also extremely volatile in March 2020, making it difficult for mortgage lenders to manage risk. In particular, lenders faced large margin calls on “to-be-announced” (TBA) forward contracts, a type of financial derivative used by lenders to hedge the mortgages held in inventory while awaiting sale. This means that lenders were forced to front up additional cash as security to their counterparties after the value of their forward positions declined. These margin calls resulted in liquidity outflows of up to $5 billion.®

The sharp economic downturn and spike in unemployment also raised the prospect of a surge in mortgage defaults and foreclosures similar to what was seen around the Great Recession in 2007–2009. Responding to the deteriorating economic situation, the federal government quickly stepped in to provide homeowner relief in the form of mortgage forbearance for borrowers facing financial difficulties, as part of the Coronavirus Aid, Relief, and Economic Security (CARES) Act signed into law on March 27, 2020.” By May, 4.7 million borrowers were in forbearance, amounting to 9 percent of all borrowers.’ But while forbearance was a lifeline for many homeowners, it created problems for some of the financial institutions servicing their loans. Mortgage servicers are typically required, at least temporarily, to forward scheduled payments to investors and other parties, even if the borrower is no longer making their mortgage payments. Forbearance was therefore a drain on the liquidity of these intermediaries.

There were particular concerns about the financial stability of nonbank mortgage companies, which today play a critical role in the mortgage market, accounting for well over half of mortgage lending as well as the majority of mortgage servicing. These firms are more exposed to liquidity risk than banks or credit unions because they rely on short-term loans (known as “warehouse lines of credit”) from financial institutions rather than deposits, and because they do not have access to the Federal Reserve discount window or other liquidity backstops.° Reflecting the risks at the time, the rating agency Moody’s switched its outlook for nonbank mortgage companies to negative at the start of April 2020, writing, “Our baseline scenario is that over the next several quarters, non-bank mortgage firms will face ongoing liquidity stress, weaker profitability, as well as declines in capitalization and asset quality.” The ultimate concern was the possibility of a liquidity crunch leading to a wave of nonbank mortgage company failures, similar to what occurred just prior to the Great Recession.” Widespread nonbank Financial distress could reduce the mortgage credit supply, with negative repercussions for the housing market and the real economy. Such an event could also reduce the quality of mortgage servicing (for example, by increasing the frequency of errors or reducing servicers’ capacity). to work with borrowers to modify their loans), potentially resulting in excessive foreclosures or other adverse outcomes for borrowers in distress. In 2022, Darren Aiello found evidence of such effects (see Security) among financialization and the constrained mortgage system. during and after the Great Recession.

What Caused the Boom?

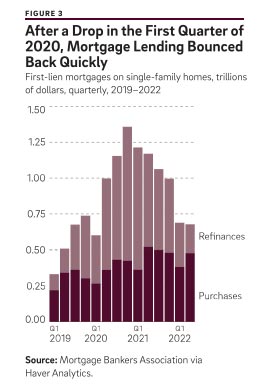

Ultimately, however, the mortgage market shook off these challenges and enjoyed a period of rapid lending growth as well as record profits for mortgage intermediaries. Figure 3 plots the quarterly evolution of lending during this period. Loan volumes grew consistently in the quarters leading up to the pandemic, reflecting falling interest rates and a solid housing market. Against this backdrop, the initial economic disruptions associated with COVID-19 are clearly apparent in the first quarter of 2020, which saw a sharp drop in lending for both purchase mortgages and refinances. But the market quickly recovered. Originations peaked in the fourth quarter of 2020 at almost $1.4 trillion, nearly double the level of the fourth quarter of the prior year. Although refinancing led the way, mortgage lending for home purchases also recovered strongly, and by the second half of 2020, it was running well above 2019 levels. What accounts for this rapid recovery and the magnitude of the credit boom? Three key factors stand out.

Government Policies

Expansionary fiscal policy and other federal government policy actions played a key role in stabilizing the mortgage market and the broader economy, particularly early in the pandemic. The CARES Act provided transfer payments to firms and to unemployed workers, supporting incomes and consumption. Mortgage forbearance prevented a wave of foreclosures that might have otherwise put downward pressure on home prices.? And actions by housing agencies helped support nonbank mortgage companies. For example, the government-sponsored enterprises Fannie Mae and Freddie Mac capped mortgage servicer advances for loans in forbearance, and Ginnie Mae created the Pass-Through Assistance Program (PTAP), a new liquidity facility for services.3

Monetary policy was also expansionary. The Federal Reserve reduced short-term interest rates to almost zero and implemented a significant new round of quantitative easing by purchasing large quantities of Treasuries and agency mortgage-backed securities (MBS). As a result, the Fed’s MBs portfolio grew rapidly during the early months of the pandemic, from $1.37 trillion in March 2020 to $1.90 trillion by early July.“

Low Interest Rates

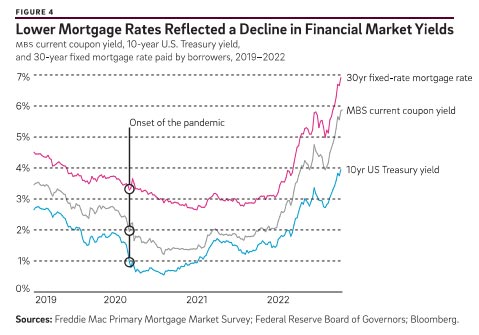

As a result of the Federal Reserve’s actions and the overall economic environment, long-term interest rates in financial markets fell significantly over the course of 2020, and lenders consequently lowered their mortgage rates (Figure 4). Mortgage interest rates are typically closely tied to MBS yields in financial markets because most loans are packaged into securities and sold to investors.

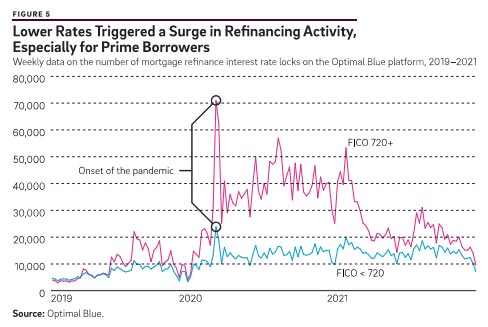

As discussed above, lower mortgage rates prompted a surge in mortgage refinancing activity. Refinancing was particularly strong for prime borrowers with high credit scores (Figure 5). The market was already primed for a period of elevated refinancing because rates had fallen significantly throughout 2019. But the further decline in rates in 2020 pushed refinancing to record levels, at least in nominal dollar terms.*

Aside from being a boon to households, the refinancing boom also provided significant support for nonbank mortgage companies through at least two channels. First, the volume of lending generated high fees and profits for mortgage lenders, strengthening their balance sheets. Second, refinancing provides a direct source of liquidity to mortgage companies because, when a borrower refinances, the money used to pay off the original loan is held in trust by the mortgage servicer for around a month before it is forwarded to MBS investors. The surge in refinancing provided a significant “float” of liquidity to mortgage companies that off- set liquidity outflows due to borrowers in forbearance not making their payments.”

Rapid Home Price Appreciation

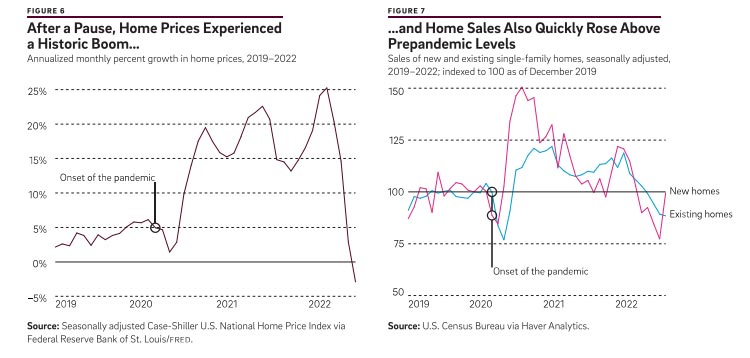

Like the mortgage market, the housing market quickly recovered as the economy stabilized and the real estate industry adjusted to the pandemic-era operating environment. In fact, home prices surged, reaching a historic annualized growth rate of around 20 percent by early 2021 (Figure 6). Lower mortgage rates contributed to this boom in prices but were not the only factor. In particular, the increase in time spent at home and the shift to remote work significantly increased the demand for residential real estate. San

Francisco Fed economist John Mondragon and University of California, San Diego, associate professor of economics Johannes Wieland estimates that the shift to remote work during the pandemic accounted for more than half of the increase in home prices in 2020–2021.” * Higher residential housing demand during this period is also evident in a sharp increase in housing rents. For example, the CoreLogic Single-Family Rent Index grew at an annualized rate of 9 percent between March 2020 and October 2021.

A hot housing market typically increases the total volume of mortgage lending, by way of three channels. First, since homebuyers are likely to finance part of the higher purchase prices through debt, the average dollar size of each mortgage generally rises. Second, rising home prices make it easier for homeowners to qualify for refinancing, and also increase home-owners ability to extract home equity through cash-out refinancing.’® Such cash-out activity did indeed become more popular during the pandemic. Third, rapid

home price growth is typically associated with a higher volume of housing transactions, increasing the number of new mortgages originated for the purpose of purchasing a home.

Regarding this third channel, home sales also quickly bounced back after dropping sharply at the start of the pandemic, with home sales exceeding pre-pandemic levels by mid-2020 (Figure 7). Sales of both new and existing homes rose, with new home sales buoyed by a boom in housing construction. This combination of robust home sales and higher home prices explains why the volume of purchase mortgages surged above pre-pandemic levels (as shown earlier in Figure 3).

Conversely, as mortgage rates have risen in 2022, the housing market boom has also subsided, reflected in a sharp drop in home price appreciation and a decline in the volume of home sales. This, in turn, has contributed to the slowdown in the volume of mortgage lending.

The Limits of the Boom

Although the 2020-21 mortgage boom was of historic proportions, a number of factors limited its scope and prevented all borrowers from fully enjoying its benefits. First, not all of the decline in financial market yields was passed through to mortgage borrowers. Although Treasury and ps yields fell sharply in March and April 2020, mortgage rates declined only gradually. Furthermore, James Vickery, one of the authors of this article, working with Philadelphia Fed senior advisor and research fellow Lauren Lambie-Hanson,

economist Andreas Fuster and several other authors estimate that the “primary-secondary” spread—the difference between mortgage rates and the relevant secondary-market MBs yield—increased by up to 100 basis points during the pan-demic, reflecting a higher “gain-on-sale” earned by lenders.”In other words, although mortgage rates reached record lows, rates would have been even lower, by as much as 1 percentage point, if lower financial market yields had been fully passed through to borrowers. Fuster, Lambie-Hanson, Vickery, et al. attribute this incomplete passthrough to the capacity constraints lenders faced. As interest rates fell, lenders experienced a dramatic increase in applications for mortgage refinances. Processing these applications and ramping up capacity

was particularly challenging due to the deteriorating economic situation, (making it difficult to accurately confirm borrower employment and income), the unexpected shift to remote work, and the wave of forbearance requests from existing borrowers. In the In the words of one mortgage company CEO in March 2020, “Lending is in a bottleneck…. Most of our correspondent buyers and wholesale buyers are discouraging new loans. They are bloated with loans in process and cannot take on any more.” Capacity constraints are a typical feature of refinancing booms, but Fuster, Lambie-Hanson, Vickery, et al. find that operational frictions rendered the credit supply unusually inelastic in 2020-2021.”

Fuster, Lambie-Hanson, Vickery, et al. also find that interest rate passthrough was even lower outside of the prime conforming mortgage market. First, mortgage rates fell by a smaller amount for jumbo mortgages, which are ineligible for government-backed credit guarantees. This likely reflects the amplification of credit risk premia during the pandemic as well as the greater difficulty of securitizing mortgages outside of the government-backed agency market. Second, interest rates were relatively elevated for mortgages sold to (typically) lower-income borrowers in the Federal Housing Administration (FHA) market. These loans carry government insurance against default, but this insurance does not fully insulate lenders from risk.” FHA loans were also at greater risk of forbearance, creating liquidity risk for mortgage intermediaries.”

Aside from these differences in interest rate pass-through, Atlanta Fed economist Kristopher Gerardi, Boston Fed economist Paul S. Willen, and Lambie-Hanson also find evidence of disparities in the extent to which borrowers were able to take advantage of lower interest rates by refinancing. In particular, they find that Black, Latino, and Asian borrowers were significantly less likely to refinance, and therefore benefited less from the low-mortgage-rate environment. Their results demonstrate a general point: Borrowers often do not refinance when it seems to be in their financial interest to do so, because of either inattention, limited financial literacy, an inability to qualify for a new loan, or other factors.*

Conclusion

The 2020-2021 period provides a valuable case study that illustrates both the strengths and the limitations of the U.S. mortgage finance system. Overcoming a variety of challenges, the mortgage market intermediated a record volume of credit, thereby supporting the housing market and providing liquidity to consumers through lower mortgage rates. But capacity constraints and other frictions limited the passthrough of lower financial market yields to mortgage borrowers. Furthermore, minority borrowers did not benefit as much as other groups from the opportunity to refinance at a lower rate.

The experience of the pandemic highlights the potential benefits of alternative mortgage designs that allow rates on existing mortgages to fall automatically with market interest rates, particularly during periods of stress. The U.S. mortgage market is dominated by long-term fixed-rate mortgages (FRMs), which require the borrower to refinance if they want to benefit from lower market rates. One alternative to this kind of market features a larger role for adjustable-rate mortgages (ARMs), as is the case in the UK, Australia, and many continental European economies. An intermediate design proposed by Boston University associate professor of economics Adam Guren and his coauthors and by Northwestern Kellogg professor of finance Janice Eberly and Stanford professor of finance Arvind Krishnamurthy is an FRM that converts to an ARM during recessions. Guren and his coauthors find that such a design would produce significant welfare benefits during economic downturns. Another variation is the ratchet mortgage advocated by finance professor Andrew Kalotay, which allows for the contract interest rate to decline but never increase.”

Looking to the future, mortgage interest rates have risen very significantly in 2022, and mortgage lending has fallen sharply as a result. Higher interest rates, assuming they persist, will be a headwind for the the housing market and presage a challenging period for the mortgage industry, which has grown in size and enjoyed record profits during the pandemic. Careful ongoing monitoring of the mortgage finance system seems warranted during this period of transition.